CRD VI – the new requirements on third-country branches: less than 12 months to go

Insight

The EU Capital Requirements Directive IV (2013/36/EU) (CRD IV) has been updated by CRD VI (2024/1619) (CRD VI) to bring in new third-country branch rules. These will apply from 11 January 2027 and will have a significant impact for UK firms, in particular UK banks, that wish to continue to provide core banking services to clients in the EU.

In this briefing we summarise the background and the key impact for UK firms of the new rules.

Background and summary

CRD VI and the Capital Requirements Regulation (2024/1623) (CRR III) were published in final form on 19 June 2024. They implement outstanding elements of the Basel III regulatory reforms and also introduce changes in other non-Basel key areas.

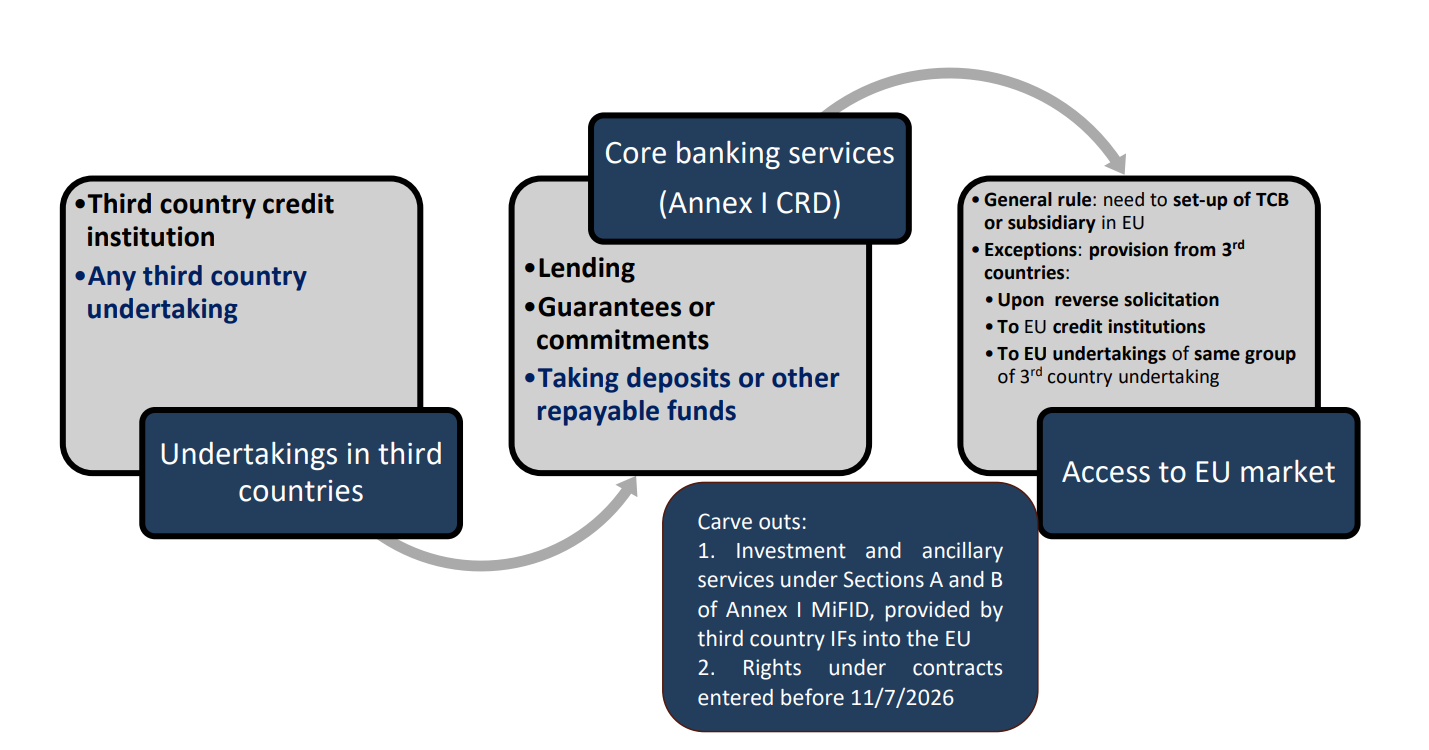

Article 21c of CRD VI provides for a harmonised EU framework for third-country firms (including UK banks) that provide core banking activities, such as deposit-taking, lending and providing guarantees, into the EU.

Under the new regime, UK banks (and other firms in scope) will no longer be permitted to provide core banking services on a cross-border basis into the EU without having a local presence, unless there is an applicable exemption or carve-out (see below for more detail).

UK banks (and other firms in scope) that wish to continue to provide core banking services into the EU within the scope of the new rules will need to establish an authorised EU branch in each member state where they operate, or set up an EU authorised subsidiary (which would be able to benefit from passporting rights). Contracts entered into before 11 July 2026 benefit from transitional provisions and can continue under current rules until they expire.

What is the rationale for the new regime?

The impetus for this new framework stems from a lack of a harmonised legal or prudential approach in the EU for the supervision of third-country branches. Currently, EU member states are only permitted to ensure that third-country branches do not benefit from more favourable treatment.

The European Commission is concerned about what it perceives as the harmful effect that such a fragmented regulatory landscape has on financial stability and market integrity within the EU. It has therefore decided to introduce this new harmonising framework.[1]

What are core banking services?

In scope, core banking services are as follows:

- taking deposits and other repayable funds;

- lending including, inter alia consumer credit, credit agreements relating to immovable property, factoring, with or without recourse, financing of commercial transactions (including forfeiting)*; and

- providing guarantees and commitments*.

*Where the firm is a credit institution or would fulfil the criteria laid down in points (i) to (iii) of Article 4(1), point (b) of CRR, if it were established in the Union. For taking of deposits and other repayable funds, the third-country branch requirement applies to any third-country undertaking.

What is the branch requirement?

Under the new rules, EU member states will have to require undertakings established in a third country that wish to commence or continue to carry out core banking activities in their member state, to establish a branch in that member state and to apply for prior authorisation of that branch. Authorisation will be contingent on the third-country firms complying with a number of regulatory requirements as described below, for example, minimum capital requirements, sufficient liquid assets and proper governance.

What about pre-existing contracts?

Contracts entered into by third-country firms before 11 July 2026 for core banking services will benefit from transitional provisions under Article 21c(5) and can continue without triggering the need to establish a branch. However, note the six-month gap between this date and 11 January 2027 when the new regime takes effect.

Are there any exemptions or carve-outs?

Yes, there are three exemptions and one carve-out to the prohibition, as follows:

| Exemption/Carve-out | Description | Comment |

| Reverse solicitation | Where a client or counterparty approaches a third-country firm at its own exclusive initiative for the provision of core banking services, including their continuation, or core banking services closely related to those originally solicited. | Does not apply if the firm solicits a client or counterparty (including potential) through an entity acting on its own behalf or having close links with the firm or through any other person acting on behalf of such firm. |

| Interbank transactions | Where the customer is a credit institution, this is not in scope. | The EBA has considered whether the interbank exemption should be expanded to include other regulated financial services firms but concluded that there was insufficient evidence to justify expansion of the exemption beyond banks. |

| Intragroup business | Where the client or counterparty is an undertaking in the same group as the third-country firm, this is also out of scope. | |

| MiFID carve-out | Investment and accommodating ancillary services under MiFID II provided by the firm. | Covers related deposit-taking or the granting of credit or loans the purpose of which is to provide MiFID services. Core banking services directly related to custody services also benefit from the carve-out. |

[Source: European Banking Authority, "REPORT UNDER ARTICLE 21C CRD6", July 2025 (EBA/REP/2025/21)]

What is the regime for third-country branches?

CRD VI introduces new authorisation and ongoing prudential, governance and reporting requirements for third party branches by replacing the existing Title VI provisions with new sub-sections in Title VI, Articles 47 - 48 CRD VI.

Classification

Third-country branches will be classified as either:

- Class 1 third-country branches with (a) booked assets in a member state equal to or greater than €5bn; or (b) which take deposits or other repayable funds from retail customers (in excess of €50m or equal to or greater than 5% of total liabilities of the third-country branch), where the head office is not in an equivalent jurisdiction or the third country is considered as a high-risk third country for AML and counter-terrorist regimes.

- Class 2 third-country branches, which fall below the thresholds for Class 1 branches. In addition, CRD VI recognises 'qualifying' branches where home‑state supervision and group prudential standards are regarded as equivalent and cooperation is strong, which may benefit from some supervisory simplification

Prudential

For all branches (with calibration by class), CRD VI introduces minimum capital endowment and local liquidity standards, intended to ensure the branch can absorb losses and manage outflows at local level. Booking and registry requirements, including the maintenance of a registry book and autonomy of EU‑booked exposures, will apply.

Reporting

There are enhanced reporting requirements for the branch and, in some respects, the head undertaking, and national competent authorities can also impose ad hoc reporting requirements.

Supervision

CRD VI significantly strengthens national competent authorities' tools in relation to third-country branches and the new rules are intended to ensure a higher degree of cooperation amongst national supervisors. If third-country branches reach a certain size, member states will be able to require them to establish a local subsidiary rather than remain as a branch.

No cross-border business

CRD VI expressly provides that third-country branches authorised in one member state will be prohibited from offering or carrying on core banking services on a cross-border basis in another member state (even if the activity is not regulated in that member state), save for transactions that are intragroup or on the basis of reverse solicitation.

Comment

The changes introduced by CRD VI represent a fundamental change for third-country firms providing core banking into the EU. Although there are some exemptions to the new rules, these are narrow in scope.

Third-country firms without an existing EU presence that provide core banking services to EU clients have been assessing their options over the last few years, including relocating those services into one or more EU branches or EU subsidiaries (which can then use the passport), or ceasing such activities altogether where they are not a material business line.

Third-country firms that already have an EU branch will need to undergo a fresh authorisation process unless the local supervisor decides to continue to recognise a pre-existing authorisation. All EU third-country branches providing core banking services will be subject to the enhanced prudential, governance and supervision regime under CRD VI. The impact will vary depending on the operating model of those branches, with those that have had light local substance being the most impacted.

[1] CRD VI - Recital (17)

This publication is a general summary of the law. It should not replace legal advice tailored to your specific circumstances.

© Farrer & Co LLP, January 2026