Artificial intelligence in tax: opportunity, risk and responsibility

Insight

This is the second article in our series focused on liability for artificial intelligence (AI) in the supply chain. Our first article provided an overview of the issues and an explanation of the broad concepts that are at play when considering who should bear responsibility for AI‑related harm.

This article explores how AI can be used in tax matters and the practical steps for managing the risks it creates.

AI and the future of tax

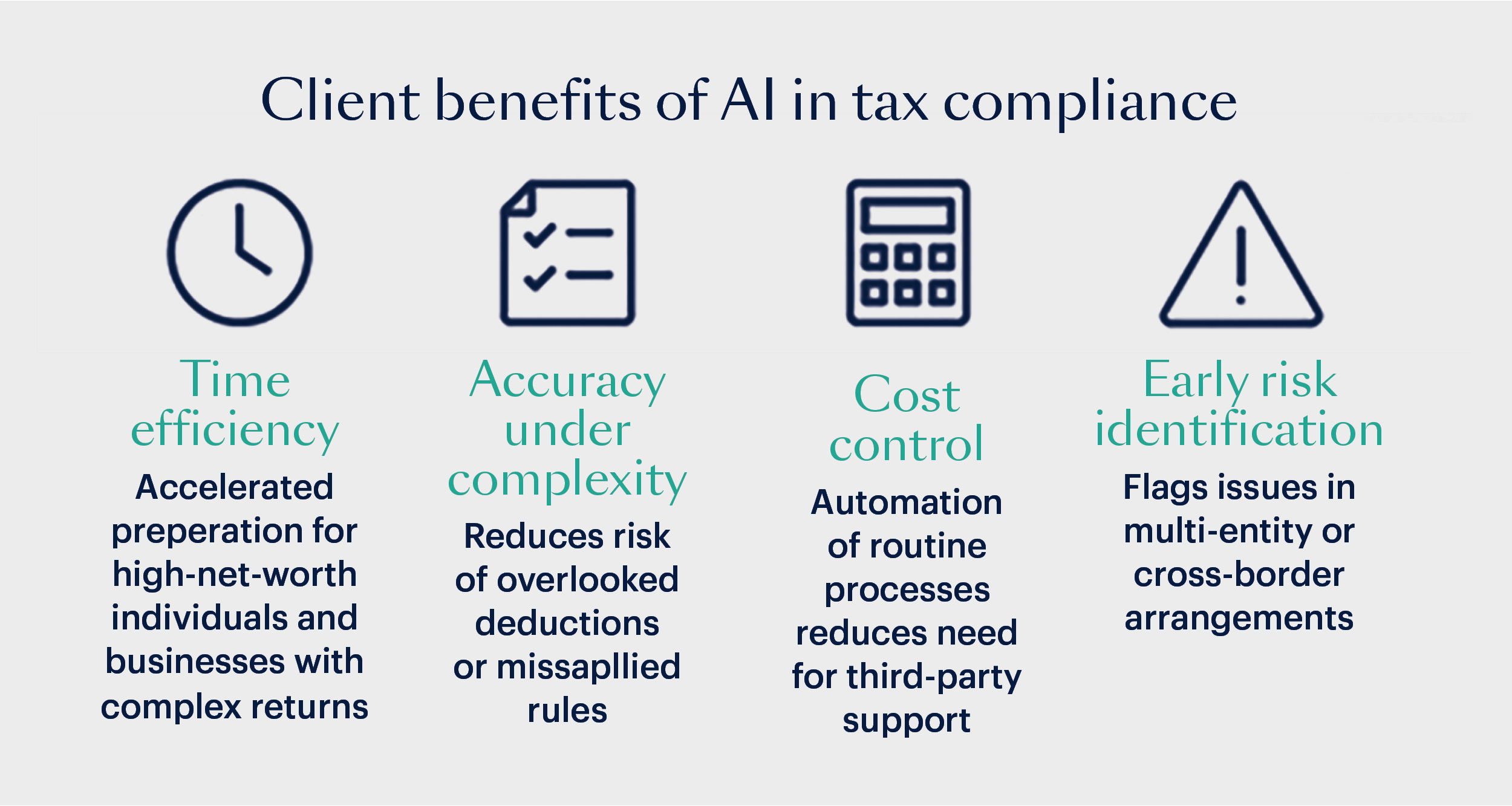

AI has the potential to revolutionise how both high-net-worth individuals and professionals approach tax. It can offer efficiencies, speed and accuracy, which may free up more time and resource for strategic advice and tax planning. Tax authorities themselves are increasingly using AI to improve operations; HMRC, for example, has reportedly been using AI to monitor social media posts to target fraudsters as part of criminal investigations into suspected tax cheats.

We set out below a few ways in which AI can be used in a tax context.

Preparation of tax returns

AI technologies can assist with the preparation of tax returns for filing. The AI programme may extract data from document sets, ingest this data into its software, and then produce an output (ie a completed tax return).

As well as being used by individuals to prepare their own tax returns (without the involvement of a professional adviser), AI may be used by advisers to streamline the process of preparing clients' tax returns. This can result in cost efficiency and potentially free up time for more valuable advisory work as opposed to more administrative tasks.

Tax advisory

By analysing data at speed, AI can help advisers understand clients’ tax positions more easily and highlight issues or opportunities early. This frees up time for better planning and risk management.

AI can support advisers in a few practical ways. For example, it can potentially help with:

- tax research: pulling together relevant legislation, guidance and commentary to give advisers a faster starting point for proper analysis;

- summarising long documents: producing first‑cut summaries of HMRC correspondence, case papers or disclosure material for review;

- organising information: arranging dates, transactions or documents into a clear timeline, which can be particularly useful in residence, domicile or enquiry matters; and

- spotting inconsistencies: flagging where facts or figures differ across drafts or documents so they can be corrected before going to HMRC.

This is a fast‑moving area, and the tools are improving quickly, so the range of tasks AI can genuinely help with is likely to grow significantly over the next few years.

What are the main risks of using AI in tax?

As discussed in our first article, when an AI system does not work as intended or promised, it is not always immediately obvious who should bear responsibility. If a taxpayer has used an AI system and/or employed a professional tax adviser, who has also used an AI system, and the amount of tax paid turns out to be wrong, who should bear liability: the taxpayer, the adviser, or the provider of the AI system(s)?

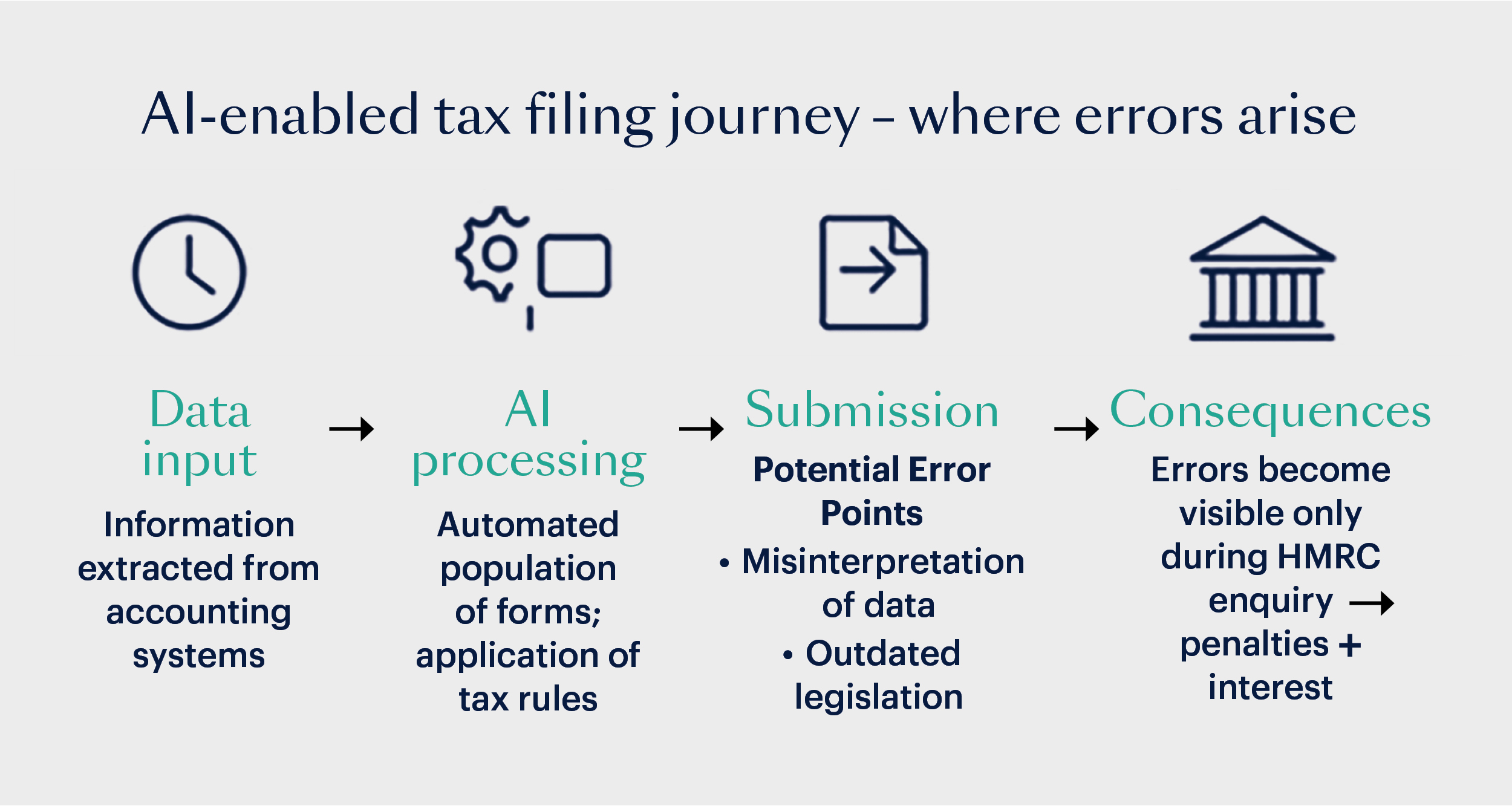

Consider a taxpayer using a major accounting firm’s AI-enabled platform. The system could use machine learning and rule based engines to extract data from accounting systems, automatically populate tax returns, and conduct real time risk analysis.

The process may feel seamless: data flows from accounting systems, forms are auto-populated, and submission occurs at the click of a button. But if the AI misinterprets data or applies outdated legislation, errors could cascade into significant tax liabilities.

Such errors may only surface much later during an HMRC enquiry, by which time interest and penalties may already be accruing.

HMRC’s position on liability and penalties

HMRC’s penalty regime is behaviour‑based and focuses on the level of care a taxpayer has taken when submitting a return. Penalties are generally grouped into three categories:

- Reasonable care: where a taxpayer has taken appropriate steps to check their return, penalties will not usually be charged.

- Careless behaviour: applies where a taxpayer fails to take reasonable care (the typical category for errors arising from unverified use of AI). Penalties range from 0% to 30% of the whole tax liability depending on disclosure and cooperation.

- Deliberate or deliberate and concealed behaviour: where a taxpayer knowingly submits an incorrect return or hides information. Penalties range from 20% to 70% for deliberate behaviour, and 30% to 100% where the behaviour is deliberate and concealed.

In a tax context, HMRC expects taxpayers to exercise reasonable care, and blind reliance on AI does not meet that standard. When AI is involved, HMRC will not treat the presence of an AI tool as evidence of reasonable care. Instead, it will assess the taxpayer’s behaviour in context: whether the output was reviewed, whether obvious anomalies were ignored, and whether the taxpayer sought clarification where needed.

Liability in a tax context: key risks to consider

Blind reliance on AI: when a taxpayer uses AI-generated output without any review, this carries an elevated risk of being categorised as careless or even deliberate behaviour. This could lead to significant penalties.

As explored during our first article, the more bespoke the AI system, the greater the likelihood that the AI provider will be liable if something goes wrong. Where the taxpayer (or an adviser) relies on a generic 'off-the-shelf' system, it will be difficult to argue that the provider of that system will be liable.

Sensible self-checking: consider a taxpayer using an AI tool to determine whether a disposal qualifies for a tax relief. The AI suggests relief applies. The taxpayer then checks HMRC’s published guidance, reviews the eligibility criteria, and records why they believe the conditions are met. If HMRC later concludes the relief was incorrectly claimed, the taxpayer’s documented steps are strong evidence of reasonable care. Although the conclusion was wrong, the behaviour demonstrates an appropriate level of diligence, meaning any penalty is likely to be reduced or not applied at all.

AI plus tax adviser: if a client relies on the advice of a professional who uses AI but still makes an error, liability generally shifts to the adviser, and a claim may be possible either through contract (if available) or for negligence. Whether the adviser can pass liability to the provider of the AI system may depend on whether the system was 'bespoke' or an 'off-the-shelf' product.

Tax advisers using AI internally: advisers may rely on AI internally to reduce costs, such as to review large volumes of client records to identify crucial factors and queries. Advisers may wish to be transparent at the outset, for example by including a section on the company and/or adviser's use of AI in their terms and conditions. However, this does not change the duty of care owed to clients. Advisers must use the same skill, care and diligence expected of a reasonably competent professional when using AI systems. This includes reviewing and checking AI outputs.

The UK Jurisdiction Taskforce on liability for AI harms

The UK Jurisdiction Taskforce’s draft legal statement on liability for AI harms notes that, over time, we may see professional negligence claims where advisers fail to use AI tools that have become established, reliable and widely adopted in their field. This does not mean that professionals owe a duty to use every new technology. Instead, the duty of care remains one of reasonable skill and judgement. Advisers must stay informed about emerging tools and use them where it is appropriate, safe and genuinely in the client’s interests. We will continue to monitor the outcomes of the final report.

In the meantime, if you or your business is considering using AI for tax-related concerns, do not hesitate to contact Farrer & Co's team of experts Ian De Freitas or Claire Randall, who can advise you on AI and tax-related concerns.

Many thanks to current solicitor apprentice Keeley Barnes for her help in writing this article.

This publication is a general summary of the law. It should not replace legal advice tailored to your specific circumstances.

© Farrer & Co LLP, February 2026