Foreign investment in UK real estate - extension of capital gains tax

Insight

From 6 April 2019 most disposals of foreign-held UK property will be subject to capital gains tax (CGT). In addition, CGT will apply to certain disposals of shares in companies that derive 75% or more of their value from UK real estate. In order to soften the blow, only capital gains which arise after the new rules take effect will be taxed.

This briefing outlines the extended CGT regime for non-resident owners of UK property.

Why is CGT being extended?

These changes form part of the British Government’s policy to align the taxation of UK and non-UK investors in UK real estate. They also bolster the tax authority’s offensive against offshore structures which are viewed as facilitating tax avoidance.

What is changing?

Previously, non-residents were taxed on disposals of UK residential property only. These were taxed under:

(i) the 2015 Non-Residents CGT rules, which applied to disposals by non-resident individuals, close companies, trusts and personal representatives, and

(ii) the Annual Tax on Enveloped Dwellings (ATED) CGT rules, which applied to disposals by companies paying the ATED charge.

From now on, subject to exceptions, a direct charge to CGT will apply to disposals of all UK property by non-resident owners, whatever the value of the property and whether it is for residential or commercial use. Further, an indirect charge to CGT will apply to certain disposals of shares in companies that are so-called ‘property rich’.

A consequence of the changes is that the ATED CGT provisions are now redundant and are abolished.

What is not changing?

The new rules do not affect the inheritance tax position with respect to non-domiciled individuals who own UK commercial property. These assets can, if the appropriate conditions are met, continue to remain outside the scope of UK inheritance tax. UK residential property will still be subject to inheritance tax whether directly or indirectly held.

Disposals of UK property which is used by the UK branch or agency of a foreign company will remain within the charge to corporation tax on capital gains.

Individuals who are resident but not domiciled in the UK can continue to claim the remittance basis with respect to the proceeds of a sale of foreign shares, even where the company is property rich under these rules.

Non-resident individual owners will still be eligible to claim the annual exempt amount with respect to their disposals. Companies can continue to make disposals intra-group on a no gain/no loss basis.

Disposals by overseas pension schemes, sovereign wealth funds and charities remain exempt from CGT.

Overlap with anti-avoidance provisions

Non-resident close companies are subject to anti-avoidance rules attributing gains to UK resident shareholders and certain other persons with an interest in the company, including the trustees of non-resident trusts. Capital gains may be further attributed to a UK resident settlor or beneficiary of a trust. The new CGT regime takes precedence over these anti avoidance provisions and there will be no double taxation, however the provisions can still apply with respect to periods of ownership prior to April 2019.

How does the CGT charge on shares work?

The following factors determine whether a disposal of shares in a property-owning company will be subject to CGT:

- The share/security type: all shares other than ‘restricted preference shares' and all loans other than ‘normal commercial loans’ are within the charge.

- Whether the company is a ‘property rich company' (see tests below).

- Whether the person making the disposal held a 25% ‘investment’ in the company (see tests below) at any time in the previous two years (other than for an insignificant period).

Note that if the share disposal is within the charge to CGT then the entire disposal will attract tax not just the proportion of value attributable to UK property.

What is a 'property rich company'?

A ‘property rich company' is a company with shares which derive at least 75% of their value from UK land (which includes all property types). This is calculated by reference to the company’s 'qualifying assets' and is traced through entities which are grouped or related. Qualifying assets are the gross assets of the company ignoring liabilities and certain intra group receivables.

What is a '25% investment’?

This is very widely defined. A shareholder will meet this test if the shareholder has the right to at least 25% of any one of the following in the company: (i) voting rights (ii) disposal proceeds (iii) distributions (iv) assets available on a winding up.

Exceptions to the CGT charge on shares

There are two exceptions to the charge on disposals of shares in a ‘property rich company'.

- The first exception is for a disposal of shares in a company which uses the property for trading purposes (eg a hospitality or retail company).

- The second exception covers a situation when a property rich company is sold at the same time as another company (or companies) which is/are not property rich. Here, the assets of all the companies being sold can be aggregated and if the combined assets do not meet the 75% property rich threshold, the share sale will not be taxed. This exemption should apply for example on the sale of a foreign group which includes a non-trading company holding UK property (eg hotels) together with a company providing services (eg hotel management).

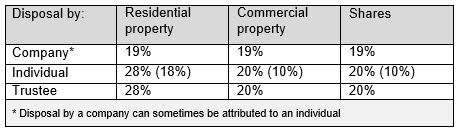

How much tax is payable?

The sweetener to the new measures is that the properties and shares which are caught are automatically rebased to their 6 April 2019 market value (unless an election is made to use the original acquisition cost). The effect of this is that only the increase in value since that date will be subject to tax.

The table below sets out the relevant tax rates.

Foreign companies holding UK property which become UK tax resident after 2019 can retain the right to a 2019 rebasing and would defer the tax until an eventual disposal. However, trusts and companies which leave the UK after 6 April 2019 will not acquire the right to a 2019 re-basing.

Non-residents' losses made by individuals/trustees are ring-fenced and can only be set off against other non-resident capital gains. Losses arising from a disposal of shares are not available for set-off.

Where a property disposal would already be taxable under 2015 Non-Resident CGT rules, those rules will continue to apply and the rebasing will be calculated by reference to the 2015 value of the property.

Reporting and payment

Unless the non-resident is already registered for self-assessment in the UK, they must file a tax return within 30 days of the transaction and pay the tax due. From April 2020 onwards all non-residents will be required to file and pay within 30 days.

Non-resident companies will now pay corporation tax rather than capital gains tax and the usual corporation tax computation rules will apply. The extension of corporation tax to income received by corporate non-resident landlords is scheduled for April 2020.

What action should I take?

Non-resident owners of UK property within the remit of the new rules should obtain a market valuation of their property as at 6 April 2019. This will ensure that following a disposal, the information required to calculate the tax charge is readily available. It is likely to be easier to obtain property valuations for 6 April 2019 now, rather than several or many years in the future. It is unfortunate that the Brexit uncertainty has kept values lower than they might otherwise have been.

Where commercial property is held by an offshore company or trust, consider whether this arrangement continues to act as a shelter from UK inheritance tax for non-UK domiciled individuals. Likewise, do shares in an offshore company remain protected from immediate tax because they are held by a shareholder claiming the remittance basis of taxation? In either of these situations, it is likely to be beneficial to keep the offshore structure in place.

In other cases, a non-UK company or non-UK trust may no longer serve its original purpose and the vehicle could be brought on-shore to the UK if doing so would reduce running costs and simplify the administration going forward. Onshoring would not affect the right to rebase the property or shares to the 6 April 2019 values.

For a general summary of the taxation of UK property held by foreign investors, see our briefing on Residential Property here and our briefing on Commercial Property here.

The new CGT rules also affect offshore investment funds holding UK real estate. You will find our briefing on Property Funds here.

This publication is a general summary of the law. It should not replace legal advice tailored to your specific circumstances.

© Farrer & Co LLP, April 2019